Market Cycles According to Howard Marks

Exploring Howard Marks' framework for investing through the ups and downs

“Superior investing doesn’t come from buying high-quality assets, but from buying when the deal is good, the price is low, the potential return is substantial, and the risk is limited.”

While reading Fundrise’s most recent shareholder letter - in which they outline their defensive positioning in the current market environment - I couldn’t help but think of Howard Marks, a renowned value investor at Oaktree Capital. He’s perhaps most famous for his memos, which are all available on Oaktree’s website. Collectively they represent decades of investing experience.

Today, I’d like to introduce you to Howard Marks, in case your unfamiliar. Then with the next post, we’ll take a look at Fundrise’s shareholder letter - I think it would make Howard Marks proud.

Who is Howard Marks?

As co-chairman of Oaktree Capital Management, Howard Marks has racked up an impressive record and along the way has shared invaluable insights in his numerous memos and books. In particular, his book Mastering the Market Cycle provides a great summation of the frameworks he’s developed over his long career. His deep understanding of these market cycles and humble perspective are at the core of his wisdom - I’ve found his memos to be both fascinating and informative.

Marks views credit cycles as a fundamental reality of the financial markets, driven by economic conditions, investor psychology, and institutional behaviors. He emphasizes that these cycles are, by their nature, unpredictable in terms of exact timing and magnitude, yet they follow a rhythmic pattern of expansion and contraction.

To emphasize: he doesn’t claim to know the timing of market bubbles and crashes. His focus is simply on identifying the stage of the cycle.

Market Cycles

“'Rule number one: Most things will prove to be cyclical. Rule number two: Some of the greatest opportunities for gain and loss come when other people forget rule number one.'“

During expansionary (growth) periods, credit is cheap and readily available. Optimism runs high and risk-taking is encouraged… but it tends to go too far.

In contrast, during contractionary periods, such as a recession, credit becomes expensive and scarce. Pessimism takes over, and most market participants want to avoid or can’t afford to take on any risk. But Marks notes that these periods of contraction, when the market is fearful and pessimistic, often provide the greatest investment opportunities.

He consistently advises against being swayed by the prevailing sentiment of the moment. Instead, he advocates for counter-cyclical investing, favoring caution when others are euphoric and finding courage when others are fearful.

“Skepticism and pessimism aren’t synonyms. Skepticism calls for pessimism when optimism is excessive. But it also calls for optimism when pessimism is excessive.”

When the market is awash with credit and optimism is too strong, it's time for smart investors to tighten their belts and become more selective. Resist the allure of easy profits and instead prioritize safe assets. When the cycle turns and credit tightens, leading to widespread fear, that's the time to look for undervalued assets and invest aggressively. It’s a contrarian approach.

“When the market is high in its cycle, investors should emphasize limiting the potential for losing money, and when the market is low in its cycle, they should emphasize reducing the risk of missing opportunity.”

Framework for Investing

So how do savvy investors implement this?

Marks identifies six components to his “formula for investing success.”

Cycle positioning—the process of deciding on the risk posture of your portfolio in response to your judgments regarding the principal cycles

Asset selection—the process of deciding which markets, market niches and specific securities or assets to overweight and underweight

If you have conviction about what stage of the market cycle you are in, it’s time to structure your portfolio accordingly. And given that the “market” is actually made up of many different markets - debt, equity, foreign, real estate, etc - this assessment informs your asset selection.

Importantly, while Marks advocates a counter-cyclical, contrarian approach, this doesn’t mean you should always do the opposite of everyone else. That almost certainly will go poorly! On this point, Marks once quoted Joel Greenblatt as saying:

“...just because no one else will jump in front of a Mack truck barreling down the highway doesn’t mean that you should.”

Instead, he advises figuring out:

what the herd is doing;

why it’s doing it;

what’s wrong, if anything, with what it’s doing; and

what you should do about it.

This process requires deep knowledge and experience with markets. And it’s good to note, most investors probably don’t have enough of either to implement this effectively.

Next, your risk posture should translate to either Aggressive or Defensive:

Aggressiveness—the assumption of increased risk: risking more of your capital; holding lower-quality assets; making investments that are more reliant on favorable macro outcomes; and/or employing financial leverage or high-beta (market-sensitive) assets and strategies

Defensiveness—the reduction of risk: investing less capital and holding cash instead; emphasizing safer assets; buying things that can do relatively well even in the absence of prosperity; and/or shunning leverage and beta

Notice it’s a spectrum, not binary. He’s not advocating moving to all cash or all gold for a defensive posture, for example. It’s about adjusting your risk tolerance.

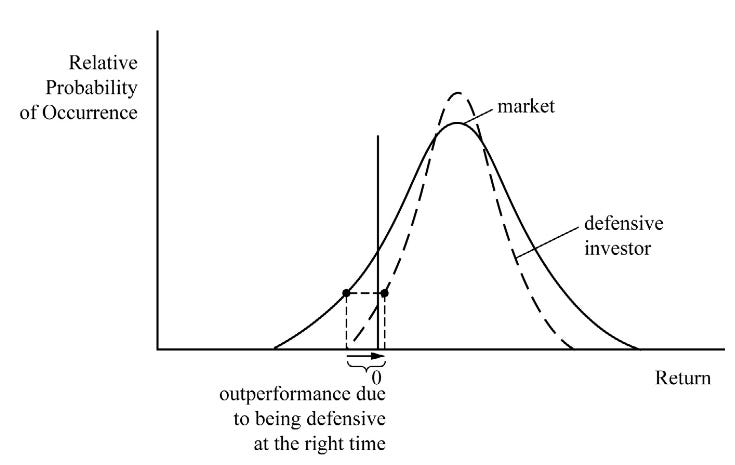

In Mastering the Market Cycle, I loved charts illustrating this.

Below is a probability distribution curve for a market’s behavior. It’s biased towards a positive return (more of the curve is to the right of 0), as markets tend to go up in the long term.

When an investor chooses to take a defensive posture, they are narrowing their probability distribution - the dashed line curve gets steeper. They are limiting their downside, as a smaller probability for loss is created. However, the upside also is also lower.

This defensive investor outperforms if the broader market suffers.

And conversely, being defensive during a market growth phase will lead to underperformance.

The final two components are Skill and Luck:

Without Skill on an investor’s part, decisions shouldn’t be expected to produce success. In fact, there’s something called negative skill, and for people who are saddled with it, flipping a coin or abstaining from decisions would lead to better results.

And Luck is the wildcard; it can make good decisions fail and bad ones succeed, but mostly in the short run. In the long run, it’s reasonable to expect skill to win out.

Acknowledging the role of skill and luck in decision-making is key. As tempting as it is, we can’t judge a decision solely based on its outcome.

Conclusion

Howard Marks' insights on market cycles and investment positioning advocate for a disciplined, counter-cyclical approach. This strategy recognizes the discernible patterns of these cycles and the pivotal role of investor sentiment.

There’s far more to learn from Marks, but we’ve at least covered a few basics.

Next post, we’ll look at the parallels with Fundrise’s current strategy.

Thanks for reading!