My Investment Portfolio (Jan 2022)

Exclusive access for my favorite readers

“Good investing isn’t necessarily about earning the highest returns, because the highest returns tend to be one-off hits that can’t be repeated. It’s about earning pretty good returns that you can stick with and which can be repeated for the longest period of time. That’s when compounding runs wild.” - Morgan Housel, The Psychology of Money

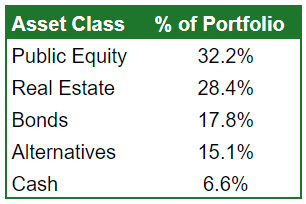

Portfolio Snapshot

To start off 2022, I decided to assess my current investment portfolio and explain my thinking behind each allocation. I’m sharing this publicly for a few reasons:

1) I don’t know how most of my peers invest their money, so maybe someone might find my approach interesting.

2) I want to document my thought process now so I can look back at this in the future… perhaps to laugh at the cryptocurrency section. (But would I laugh because I put too much or too little in it?)

I’m always in learning mode and know that my investing philosophy will continue evolving. Part of my learning mode has led me to try out a variety of investments to the point where I might be too diversified. But I’m OK with that. Better to experiment early and find what works for me while I have a long time horizon to figure it out.

Introduction to the Portfolio

This is my entire non-retirement investment portfolio - no 401ks or IRAs. Some of these investments are in tax-advantaged accounts, such as HSAs and 529 plans. I did not include my checking or savings accounts for this analysis.

I do not use leverage. That’s always been a bad word from my perspective. I am researching strategies which use leverage for investment efficiency purposes rather than concentrated bets, but that’s a newsletter for another day!

I would score my current portfolio risk level as moderate. Probably a 6 out of 10. Although, when I heard an acquaintance was moving their savings into crypto, I began to wonder if my scale was broken…

My Portfolio Overview

I narrowed down the investments into five categories: Public Equity, Real Estate, Alternatives, Bonds, and Cash.

Side Note: I recently read Phil Huber’s The Allocator’s Edge: A Modern Guide to Alternative Investment and the Future of Diversification and was pleased to realize my portfolio, if you squint hard enough, had some of the characteristics of his adapted 60/40 portfolio. But I’ll save that for yet another post..

Public Equity: 32.2%

Global Asset Allocation (GAA) and Avantis ETFs

Why: Investing in the stock market is one of the purest, most traditional ways to build wealth. My goal is to ride the ever-growing global economy through the ups and downs.

What’s in here: I utilize ETFs rather than picking individual stocks. My ‘core’ allocation is to the Global Asset Allocation (GAA) ETF, which I wrote about previously. This ETF is about 60% equity, most of which is via a global ‘Shareholder Yield’ factor tilt. Shareholder yield looks at how much a company pays in dividends plus net share repurchases (aka “buybacks”). At a high level, this tends to favor companies which screen for Value and Quality factors.

“As an example, if a company spent $3 billion on dividends and $4 billion on share repurchases, but issued $1 billion worth of shares, then the total amount spent on dividends and net share repurchases was $6 billion. If the market capitalization of the company is $100 billion, then the shareholder yield is 6%.” (link)

To increase the equity exposure beyond what GAA provides, I use Avantis ETFs such as AVUS (US) and AVDE (developed markets ex-US). These are broadly diversified across different company sizes and industries, with a slight tilt to Value. The top holdings in the AVUS (US) fund are Apple, Microsoft, Amazon, Meta, and Alphabet - similar to what an S&P 500 fund would hold, but with these companies at a lower percentage allocation.

Real Estate: 28.4%

Fundrise, Groundfloor, Steward, Public REITs

Why: We all interact with real estate daily - for me, there’s added confidence in investing in such a ubiquitous and necessary asset class. With real estate, you get a consistent winner historically, along with diversification benefits relative to equities - a nice combo.

“There is a tangibility and realness that accompanies it—the homes we reside in, the office buildings we work in, the hotels we stay in and the stores we shop in.” - Phil Huber, The Allocator’s Edge

What’s in here: The majority of this bucket is allocated to Fundrise, one of the premier real estate crowdfunding platforms. Within Fundrise, I’ve chosen the most aggressive strategy, called “Opportunistic”, which has a risk/return profile more similar to equities than other income-oriented real estate strategies (see below). Check out this podcast interview with Fundrise CEO Ben Miller for more info on their Sunbelt / build-to-rent residential real estate strategy.

Groundfloor allows investors to “fund short-term, high-yield loans to "flippers" -- borrowers who use short-term debt to buy a distressed property, fix it up, and either refinance it as a rental or resell it for a profit” (Link). It’s a combination of peer-to-peer lending and real estate finance. Groundfloor is constantly adding new deals and you can invest in $10 increments, which allows you to diversify across a range of options. I’ve enjoyed following some of the projects I invested in and would score them as moderate to high risk.

Farmland is a big asset class getting more attention these days as a potential inflation hedge. It’s hard for non-accredited investors to get decent exposure here, but I’ve opted for a small allocation to Steward. They provide crowdfunded loans to private farms across the US. Investors get regular updates from the farmers about the renovations and upgrades enabled by the loan.

And finally, I have exposure to a few public REITs, mostly via the Global Asset Allocation (GAA) ETF covered in my previous post.

Bonds: 17.8%

Diversified Bond ETFs via GAA, I-Bonds

Why: While bonds are offering very low yields today, they historically tend to have low to negative correlation with stocks. That relationship has been called into question in recent years, but for now I’m comfortable with a diversified bond allocation. (The Allocator’s Edge is all about the need for Alternative Assets to supplement/replace the traditional role of bonds). Beyond this, I-Bonds in particular are a great option given inflation concerns.

What’s in here: A very broad array of bonds ETFs primarily sourced through the Global Asset Allocation (GAA) ETF, which includes US treasuries, emerging markets high yield bonds, corporate bonds, and more.

In 2021, I also began purchasing I-Bonds. These US government bonds provide a base rate (currently 0%) with an additional inflation-linked rate via the Consumer Price Index (CPI) that is adjusted every 6 months. As a result of recent elevated inflation, right now these bonds offer a 7.12% yield for the first six months you own them. There are some limitations to keep in mind, such as a 1 year lock on accessing your deposit and a $10k/year cap on the amount of I-Bonds you can purchase. It’s a pretty great deal for now! (TreasuryDirect)

Alternatives: 15.1%

Crypto, Eco, Wine

Why: As outlined in my previous post on alternative investments, this broad range of assets can provide great diversification for a portfolio. This is also a fun category, in my opinion, and one I plan to continue expanding given the right opportunities.

What’s in here: Riding the cryptocurrency rollercoaster is quite the experience! I also think it’s important to note the incredible breadth of this category. First, you have the blue-chip assets, such as Bitcoin and Ethereum. Then, your altcoins like Solana, Cosmos, The Graph, etc. And finally, your meme/joke coins, of which there is a never ending supply - this is purely gambling from my perspective.

I’m most interested in DeFi (Decentralized Finance) and blockchain infrastructure, so my top 5 holdings are Ethereum, Solana, Chainlink, The Graph, and Cosmos. There are some interesting crypto indexing products launching soon which I’ll also consider - I don’t plan to invest the time and effort in becoming anything close to a blockchain expert, but I want exposure to this space. I primarily use Coinbase, but have a few wallets as well.

Eco is “one simple balance that lets you spend, send, save and make money at the same time.” (referral link) I’m currently earning 3% APY on my account and get 5% cashback on all Amazon purchases. They invest your money in stablecoins which provide liquidity to cryptocurrency markets - it’s not without risk. They are also not FDIC-insured, as they do not want the associated regulations with being a bank. So why do I bother? It’s a small allocation for my portfolio and I am not naïve regarding the risks; however, as an early user I’m earning lots of Eco points (think of them as credit card points) which have upside if Eco becomes successful. It’s fun to be early and see where this goes.

Beyond crypto, I also have a small allocation to fine wine via Vinovest. They purchased a case of Chateau Rauzan-segla 2eme Cru Classe on my behalf, which I’m hoping ages beautifully despite my inability to pronounce it.

Cash: 6.6%

Why: This is primarily for maintaining flexibility as opportunities arise, as well as reducing volatility. In addition, I can use cash to rebalance my portfolio (buying under-performing assets) instead of having to sell high-performing assets and potentially creating a taxable event.

What’s in here: $$$. It’s just cash.

There’s my personal portfolio. What do you think? Any suggestions? Let me know via email or the comment section.

I’m currently developing a formal investing plan - up to this point, it has all lived in my head. But for plenty of behavioral science reasons, I know officially documenting my values, goals, and strategy will help protect me from myself.

Thanks for reading!

Great post! I need to get my real estate game up.

Excellent post.